From payment transactions to private market financing, blockchain is changing every aspect of Wall Street. Seeing that the blockchain is growing and growing, will the traditional banking industry accept this emerging technology, or will it be replaced by it?

Last September, JPMorgan Chase CEO Jamie Dimon gave Bitcoin a head start, saying it was worse than the Dutch tulip bubble and would not have a good result. Someone will lose their lives.

After Dimon’s anger, Lloyd Blanke, the CEO of another Wall Street giant, Goldman Sachs, also responded with “some things (overnight) fluctuating by 20%, which doesn’t feel like money, but a line The tool of cheating."

At the same time, a survey by the International Securities Institutions Trade and Communications Association (ISITC) found that 55% of companies surveyed are monitoring or researching blockchains or developing solutions based on blockchain.

However, Wall Street’s public slamming of encrypted digital currencies raises the question: What exactly is the banking industry afraid of cryptocurrency?

The answer is simple: a lot of things.

Because blockchain technology provides an encrypted and secure way to deliver digital assets, it does not require trusted third parties such as banks. What's more, tools like smart contracts promise customers that they can automate multiple processes that can be completed in a long time in the banking industry, from tax compliance and reporting services to distributing property based on wills, involving multiple businesses.

The global banking industry is currently a $134 trillion industry. Banks help to complete intermediation payments, issue loans, and assess credit for borrowers. As a technology that eliminates the intermediary process in an untrusted environment, the blockchain is expected to subvert the following areas of the banking industry:

1. Payment : Blockchain technology can eliminate the need for intermediaries to approve transactions between consumers, may speed up payments, and is lower than the bank charges.

2. Clearing and settlement systems: Blockchain technology and distributed ledgers can reduce operating costs and bring us closer to the level of real-time transactions between financial institutions.

3. Fundraising: Through the initial issuance of tokens (ICO), the blockchain provides some industries with rapid access to liquidity, creating a new type of encryption economy financing model without facing the capital threshold of any traditional financial services. .

4. Securities: The blockchain subverts the financial market structure by using traditional securities such as stocks, bonds and some alternative assets in tokens.

5. Credit: Blockchain allows the credit industry to manage without caregivers, making loans safer and offering lower interest rates.

The chain has to sort out some of the research data and conclusions on CBInsight. This article will delve into how the blockchain may subvert the traditional banking industry and implement some new business models through technology.

PayWe also need an old system to support the trillions of dollars in global flows. This system is not only slow to pay, but also an additional fee.

Suppose you work in San Francisco, USA, and want to send some of your income to family members living in London. If you choose to wire transfer, you may have to pay a fixed fee of $25, and the associated extra charges may be up to 7% of the remittance amount. The bank that remits your income will be charged a certain amount. The bank that collects money from London will also deduct a sum. You have to bear some hidden losses for the US dollar to exchange for the British pound. Even after this layer of charge, your family's receiving bank will have to wait a week to register for the transaction.

The cost of each transfer transaction is usually 7.68% of the transfer amount, and transaction charges are related to payment, such as wire transfer fees or hidden losses of exchange rate exchange. For banks, the benefits of facilitating payments to complete such businesses are lucrative, and they have little incentive to reduce related fees. In 2016, from payments to letters of credit, revenue from various cross-border payment transactions accounted for 40% of the total revenue from banking global payments.

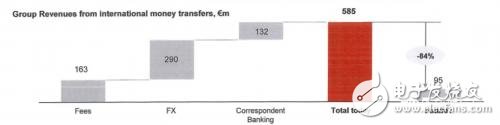

The picture above is from an internal file of the leaked Santander Bank of Spain. The screenshot section shows the revenue generated by the international money transfer business for the bank and the risks that the bank faces in the blockchain subversion. Nearly 10% of Santander's revenue in 2016 came from international transfers.

The blockchain provides a safer, lower-cost point-to-point (P2P) payment method that eliminates the need for a transfer intermediary and overturns existing systems. Because encrypted digital currencies such as Bitcoin and Ethereum are based on a common decentralized ledger, anyone can transfer and collect money through them, reducing the need for trusted third-party verification transactions.

Blockchain technology allows people around the world to pay without being bound by any borders, making payments quickly and cost-effective, no matter where they are.

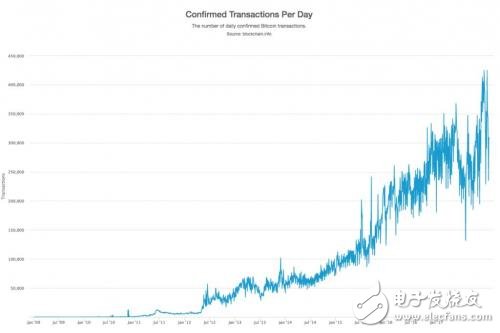

The average daily trading volume of confirmed Bitcoin has doubled, from more than 50,000 in the summer of 2014 to more than 400,000 in 2018.

Due to the high transaction costs, developers are actively expanding the range of low-cost solutions by using cryptocurrencies such as Bitcoin and Ethereum. Cryptographic currencies such as Bitcoin cash are already contributing to low-priced transactions. Currently, the transaction fee for Bitcoin cash is approximately $0.20 per transaction.

A company called TenX is addressing the above cross-border payment issues in a slightly different way. The company introduced a wallet linked to a debit card to allow cardholders to use cryptocurrency. As long as the debit card can be used normally, the cryptocurrency can be consumed by any user. The company built a distributed network for trading between different cryptocurrencies and combined the network with physical debit cards.

As a payment intermediary, there is still a long way to go before cryptocurrencies can completely replace legal currency. The volume of cryptocurrencies such as Bitcoin and Ethereum has grown exponentially over the past few years. In 2016 alone, Bitcoin’s trading volume increased by 118%, but many of these transactions were speculative and not P2P payments.

Today, the blockchain is expected to provide financial services to the billions of developing countries around the world. BitPesa is a realistic example. The blockchain company focuses on increasing inter-enterprise (B2B) payments in developing countries such as Kenya, Nigeria, and Uganda, with an average monthly transaction volume of $10 million. The average rate of traditional cross-border payments in Kenya is 9.2%, and BitPesa can reduce costs to 3% through blockchain technology.

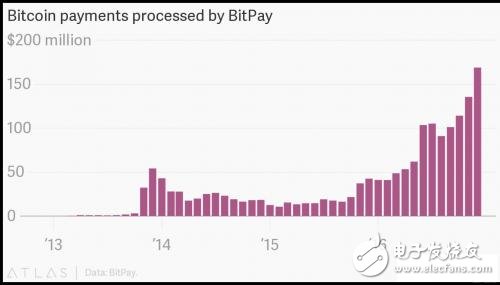

In the past few years, the amount of payment transactions handled by Bitcoin payment processor BitPay has soared.

Another example is bitcoin payment service provider BitPay. The company helps merchants accept payments in the form of bitcoins and store these payments. Last year, BitPay's payment transaction volume surged by 328%, and merchants received an average monthly payment of more than $110 million. BitPay charges 1% for each transaction, while traditional credit card transactions charge 2-3%.

An important reason for the blockchain's imminent subversion of payments is that the infrastructure supporting this area is already faltering and the entire clearing and settlement system is easily overturned.

Clearing and settlement systemBank transfers typically take three days to settle, which is largely related to how the financial infrastructure is built.

This is not only painful for consumers. For banks, global transfers are also a nightmare for logistics.

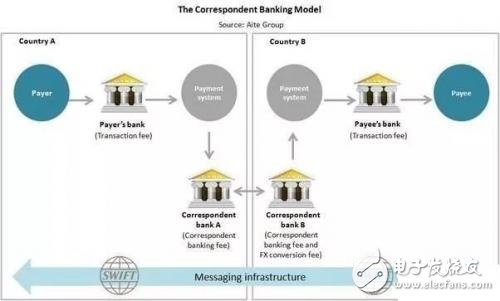

Today, if a bank wants to complete a simple inter-account transfer, it must circumvent a complex intermediary system such as correspondent banking and hosted services before the money reaches any destination. Otherwise, the accounts of the two banks must meet the requirements of the global financial system and obey a large network of traders, funds, and asset managers.

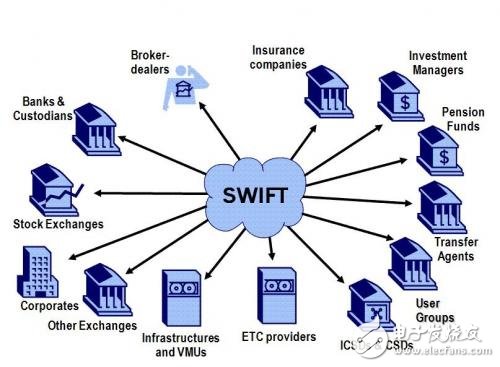

If you want to transfer money from the account of Italy's Yuxin Bank to Wells Fargo's account, the transaction will be carried out through the SWIFT, which delivers 24 million messages per day to 10,000 financial institutions.

Because Yuxin Bank and Wells Fargo did not establish a financial business relationship, they must find a correspondent bank in SWIFT's network that has business relations with both banks and can settle transactions. The agency bank charges for this service. Each agent bank has different book records at both the export bank and the receiving bank, and ultimately these different records must be unified.

The centralized SWIFT protocol did not actually issue remittances, but only sent payment instructions. The remittance is actually handled through an intermediary system. Each intermediary will increase transaction costs and may result in a transfer failure. 60% of B2B payments require human intervention, and each intervention takes 15 to 20 minutes.

The blockchain acts as a decentralized transaction book that completely overturns the above clearing and settlement system. The blockchain between banks does not need to use SWIFT to achieve the uniformity of all financial institutions' books, but it is possible to track all transactions transparently and transparently. This means that transactions do not have to rely on managed services and proxy lines, and transactions can be settled directly in the blockchain. This will help reduce the high cost of maintaining a global correspondent bank network.

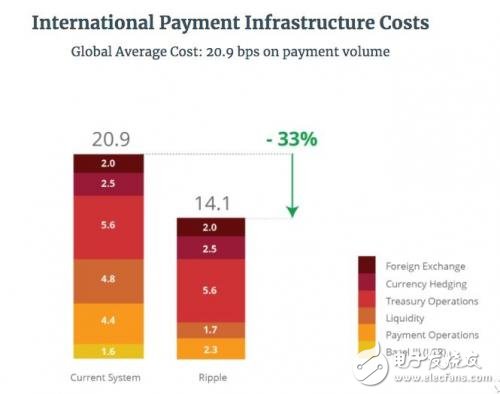

Some banks estimate that blockchain innovation could reduce the cost of the financial industry by at least $20 billion by providing better settlement and clearing infrastructure.

Ripple, the company that provides enterprise blockchain services, is trying to replace SWIFT. Ripple is best known for its internal network of Ripple (XRP), but this cryptocurrency has nothing to do with Ripple's banking products.

The message sent by SWIFT is one-way, much like an email. This means that the transaction can be settled after both the export and receipt lines receive the transaction instructions. Ripple's product, xCurrent, directly integrates the bank's existing books, providing banks with a faster two-way communication protocol that allows for real-time messaging and billing. Ripple is currently contracting with more than 100 customers to collaborate with the Ripple blockchain network for this experimental settlement.

15Inch Woofer,15 Inch Woofer,15 Inch Loudspeaker,Carbon Fiber Woofer

Guangzhou BMY Electronic Limited company , https://www.bmy-speakers.com