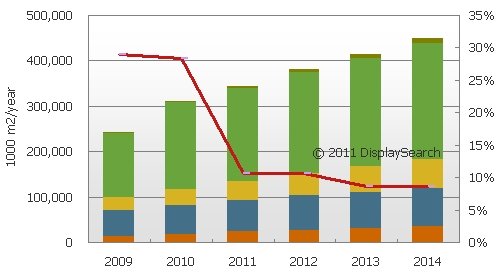

According to the latest DisplaySearch forecast, as the replacement of flat-panel TVs is almost completed, the demand for LCD TV panels will slow down. The growth rate in 2010 will be as high as 41%, and in 2011 it will decline to 8.3%. In 2011, the demand area of ​​the entire TFT-LCD panel is expected to increase by 10.4%, which will drive the demand for TFT-LCD glass by 11%.

According to the latest DisplaySearch forecast, as the replacement of flat-panel TVs is almost completed, the demand for LCD TV panels will slow down. The growth rate in 2010 will be as high as 41%, and in 2011 it will decline to 8.3%. In 2011, the demand area of ​​the entire TFT-LCD panel is expected to increase by 10.4%, which will drive the demand for TFT-LCD glass by 11%. Due to the tight market supply in 2009, TFT-LCD glass substrate suppliers substantially expanded their production capacity in 2010, and the supply area increased by 32% year-on-year. It is expected that it will grow by 13% in 2011. However, as many panel makers reduced capacity utilization in the first quarter, it is estimated that the supply of glass substrates will exceed demand in the first quarter of 2011, and supply will be about 12.8% higher than demand.

As the investment in new glass furnaces is extremely expensive, most of the recent increase in production capacity has come from increasing the capacity of existing furnaces, increasing the yield rate, and accelerating the production process. For manufacturers using Fusion's production processes, the main way to increase productivity is to produce thinner glass substrates, especially in the sixth generation line and higher generation line 0.5mm, replacing the original 0.7mm. It is estimated that from the second quarter of 2009 to the second quarter of 2011, the TFT-LCD glass production capacity will increase by 42%, and the number of glass furnaces will increase by 15%.

Since the market began to improve in the second quarter of 2009, glass substrate manufacturers have different production capacity expansion strategies. The top three manufacturers are Corning (including Corning and South Korea's Samsung Corning), Asahi Glass and NEG. Among them, Corning gave up part of the TFT-LCD market share and transferred some of its production capacity to Gorilla Glass. The market share of Samsung Corning and Asahi Glass remained basically the same as before, while NEG continued to increase market share.